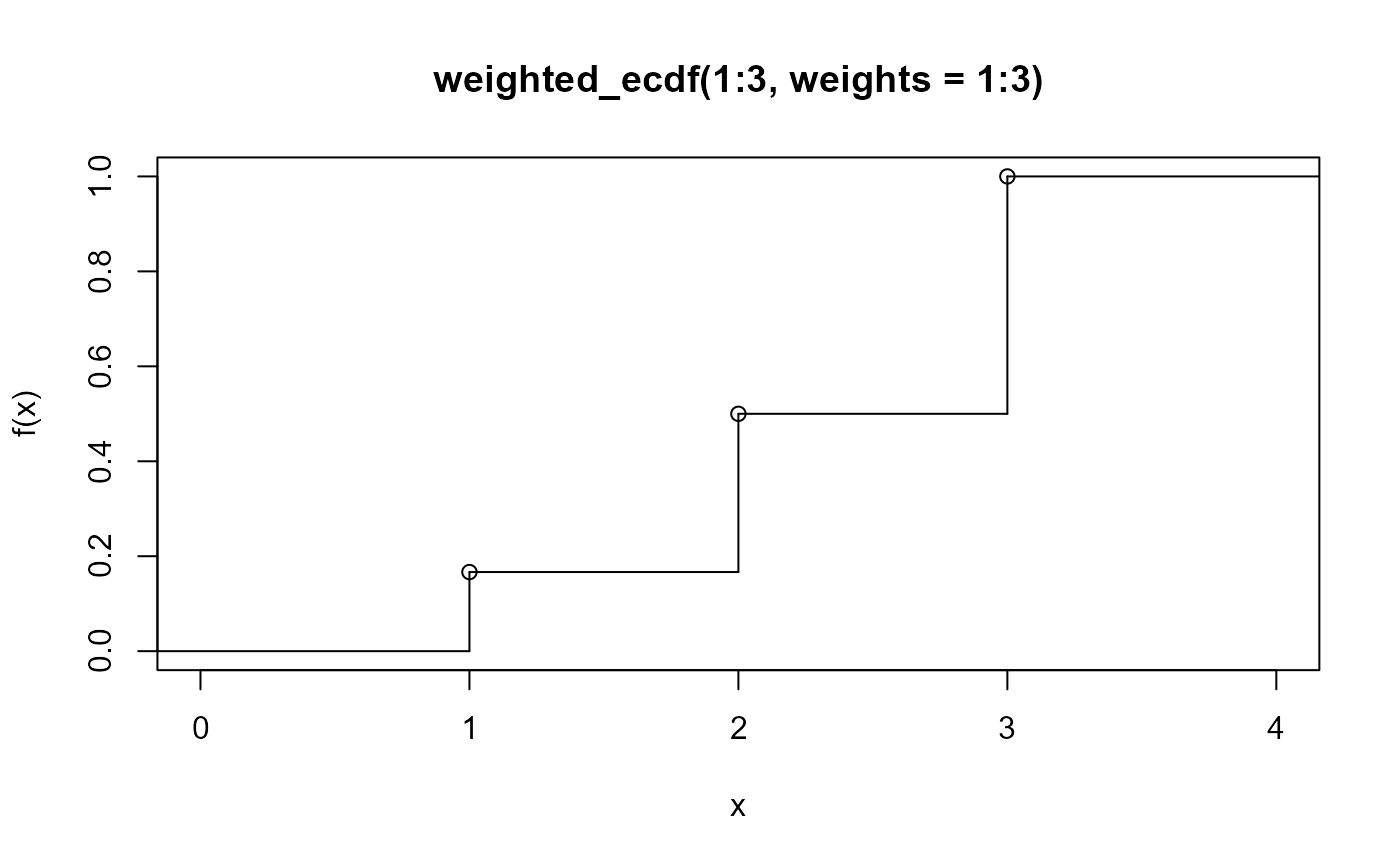

A variation of ecdf() that can be applied to weighted samples.

Arguments

- x

<numeric> Sample values.

- weights

<numeric | NULL> Weights for the sample. One of:

numeric vector of same length as

x: weights for corresponding values inx, which will be normalized to sum to 1.NULL: indicates no weights are provided, so the unweighted empirical cumulative distribution function (equivalent toecdf()) is returned.

- na.rm

<scalar logical> If

TRUE, corresponding entries inxandweightsare removed if either isNA.

Value

weighted_ecdf() returns a function of class "weighted_ecdf", which also

inherits from the stepfun() class. Thus, it also has plot() and print()

methods. Like ecdf(), weighted_ecdf() also provides a quantile() method,

which dispatches to weighted_quantile().

Details

Generates a weighted empirical cumulative distribution function, \(F(x)\).

Given \(x\), a sorted vector (derived from x), and \(w_i\), the corresponding

weight for \(x_i\), \(F(x)\) is a step function with steps at each \(x_i\)

with \(F(x_i)\) equal to the sum of all weights up to and including \(w_i\).